Multiple Comparisons¶

This setup code is required to run in an IPython notebook

[1]:

import matplotlib.pyplot as plt

import seaborn as sns

sns.set_style("darkgrid")

plt.rc("figure", figsize=(16, 6))

plt.rc("savefig", dpi=90)

plt.rc("font", family="sans-serif")

plt.rc("font", size=14)

[2]:

# Reproducability

import numpy as np

gen = np.random.default_rng(23456)

# Common seed used throughout

seed = gen.integers(0, 2**31 - 1)

The multiple comparison procedures all allow for examining aspects of superior predictive ability. There are three available:

SPA- The test of Superior Predictive Ability, also known as the Reality Check (and accessible asRealityCheck) or the bootstrap data snooper, examines whether any model in a set of models can outperform a benchmark.StepM- The stepwise multiple testing procedure uses sequential testing to determine which models are superior to a benchmark.MCS- The model confidence set which computes the set of models which with performance indistinguishable from others in the set.

All procedures take losses as inputs. That is, smaller values are preferred to larger values. This is common when evaluating forecasting models where the loss function is usually defined as a positive function of the forecast error that is increasing in the absolute error. Leading examples are Mean Square Error (MSE) and Mean Absolute Deviation (MAD).

The test of Superior Predictive Ability (SPA)¶

This procedure requires a \(t\)-element array of benchmark losses and a \(t\) by \(k\)-element array of model losses. The null hypothesis is that no model is better than the benchmark, or

where \(L_i\) is the loss from model \(i\) and \(L_{bm}\) is the loss from the benchmark model.

This procedure is normally used when there are many competing forecasting models such as in the study of technical trading rules. The example below will make use of a set of models which are all equivalently good to a benchmark model and will serve as a size study.

Study Design¶

The study will make use of a measurement error in predictors to produce a large set of correlated variables that all have equal expected MSE. The benchmark will have identical measurement error and so all models have the same expected loss, although will have different forecasts.

The first block computed the series to be forecast.

[3]:

import statsmodels.api as sm

from numpy.random import randn

t = 1000

factors = randn(t, 3)

beta = np.array([1, 0.5, 0.1])

e = randn(t)

y = factors.dot(beta)

The next block computes the benchmark factors and the model factors by contaminating the original factors with noise. The models are estimated on the first 500 observations and predictions are made for the second 500. Finally, losses are constructed from these predictions.

[4]:

# Measurement noise

bm_factors = factors + randn(t, 3)

# Fit using first half, predict second half

bm_beta = sm.OLS(y[:500], bm_factors[:500]).fit().params

# MSE loss

bm_losses = (y[500:] - bm_factors[500:].dot(bm_beta)) ** 2.0

# Number of models

k = 500

model_factors = np.zeros((k, t, 3))

model_losses = np.zeros((500, k))

for i in range(k):

# Add measurement noise

model_factors[i] = factors + randn(1000, 3)

# Compute regression parameters

model_beta = sm.OLS(y[:500], model_factors[i, :500]).fit().params

# Prediction and losses

model_losses[:, i] = (y[500:] - model_factors[i, 500:].dot(model_beta)) ** 2.0

Finally the SPA can be used. The SPA requires the losses from the benchmark and the models as inputs. Other inputs allow the bootstrap sued to be changed or for various options regarding studentization of the losses. compute does the real work, and then pvalues contains the probability that the null is true given the realizations.

In this case, one would not reject. The three p-values correspond to different re-centerings of the losses. In general, the consistent p-value should be used. It should always be the case that

See the original papers for more details.

[5]:

from arch.bootstrap import SPA

spa = SPA(bm_losses, model_losses, seed=seed)

spa.compute()

spa.pvalues

[5]:

lower 0.273

consistent 0.320

upper 0.322

dtype: float64

The same blocks can be repeated to perform a simulation study. Here I only use 100 replications since this should complete in a reasonable amount of time. Also I set reps=250 to limit the number of bootstrap replications in each application of the SPA (the default is a more reasonable 1000).

[6]:

# Save the pvalues

pvalues = []

b = 100

seeds = gen.integers(0, 2**31 - 1, b)

# Repeat 100 times

for j in range(b):

if j % 10 == 0:

print(j)

factors = randn(t, 3)

beta = np.array([1, 0.5, 0.1])

e = randn(t)

y = factors.dot(beta)

# Measurement noise

bm_factors = factors + randn(t, 3)

# Fit using first half, predict second half

bm_beta = sm.OLS(y[:500], bm_factors[:500]).fit().params

# MSE loss

bm_losses = (y[500:] - bm_factors[500:].dot(bm_beta)) ** 2.0

# Number of models

k = 500

model_factors = np.zeros((k, t, 3))

model_losses = np.zeros((500, k))

for i in range(k):

model_factors[i] = factors + randn(1000, 3)

model_beta = sm.OLS(y[:500], model_factors[i, :500]).fit().params

# MSE loss

model_losses[:, i] = (y[500:] - model_factors[i, 500:].dot(model_beta)) ** 2.0

# Lower the bootstrap replications to 250

spa = SPA(bm_losses, model_losses, reps=250, seed=seeds[j])

spa.compute()

pvalues.append(spa.pvalues)

0

10

20

30

40

50

60

70

80

90

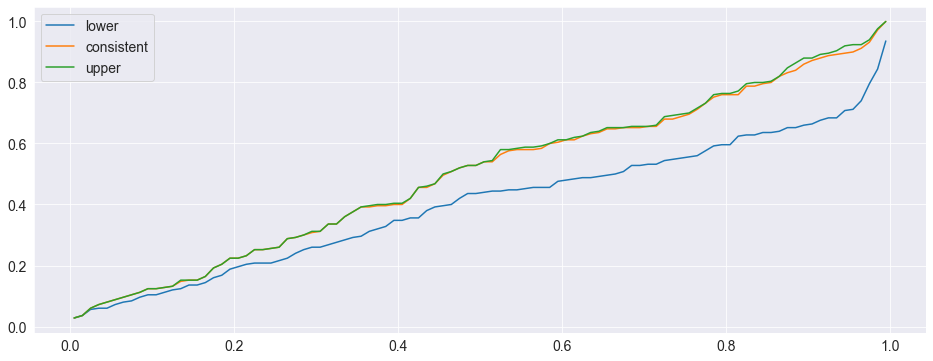

Finally the pvalues can be plotted. Ideally they should form a \(45^o\) line indicating the size is correct. Both the consistent and upper perform well. The lower has too many small p-values.

[7]:

import pandas as pd

pvalues_df = pd.DataFrame(pvalues)

for col in pvalues_df:

values = pvalues_df[col].to_numpy(copy=True)

values.sort()

pvalues_df[col] = values

# Change the index so that the x-values are between 0 and 1

pvalues_df.index = pd.Index(np.linspace(0.005, 0.995, 100))

fig = pvalues_df.plot()

Power¶

The SPA also has power to reject then the null is violated. The simulation will be modified so that the amount of measurement error differs across models, and so that some models are actually better than the benchmark. The p-values should be small indicating rejection of the null.

[8]:

# Number of models

k = 500

model_factors = np.zeros((k, t, 3))

model_losses = np.zeros((500, k))

for i in range(k):

scale = (2500.0 - i) / 2500.0

model_factors[i] = factors + scale * randn(1000, 3)

model_beta = sm.OLS(y[:500], model_factors[i, :500]).fit().params

# MSE loss

model_losses[:, i] = (y[500:] - model_factors[i, 500:].dot(model_beta)) ** 2.0

spa = SPA(bm_losses, model_losses, seed=seed)

spa.compute()

spa.pvalues

[8]:

lower 0.003

consistent 0.003

upper 0.003

dtype: float64

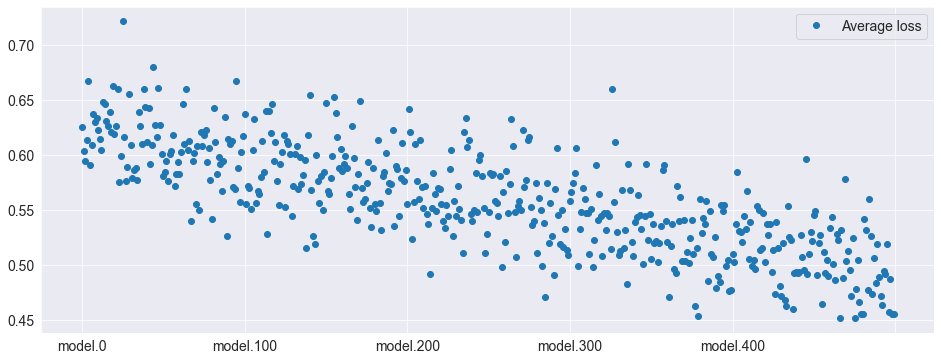

Here the average losses are plotted. The higher index models are clearly better than the lower index models – and the benchmark model (which is identical to model.0).

[9]:

model_losses_df = pd.DataFrame(

model_losses, columns=["model." + str(i) for i in range(k)]

)

avg_model_losses = pd.DataFrame(model_losses_df.mean(axis=0), columns=["Average loss"])

fig = avg_model_losses.plot(style=["o"])

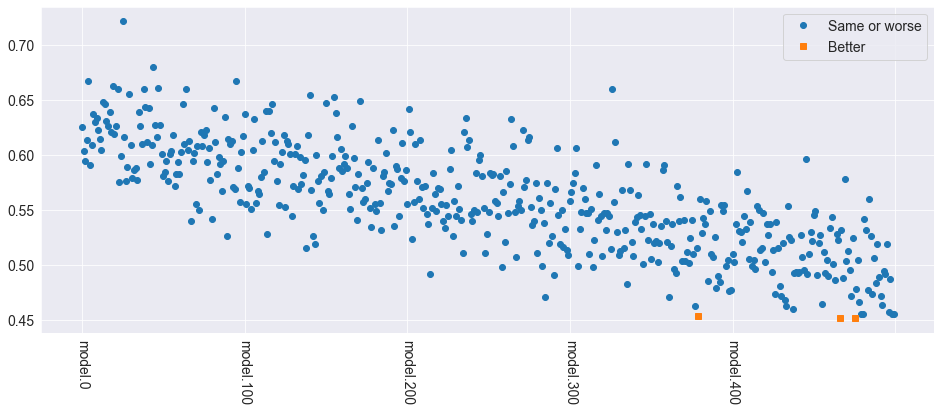

Stepwise Multiple Testing (StepM)¶

Stepwise Multiple Testing is similar to the SPA and has the same null. The primary difference is that it identifies the set of models which are better than the benchmark, rather than just asking the basic question if any model is better.

[10]:

from arch.bootstrap import StepM

stepm = StepM(bm_losses, model_losses_df)

stepm.compute()

print("Model indices:")

print([model.split(".")[1] for model in stepm.superior_models])

Model indices:

['248', '342', '353', '377', '390', '392', '411', '416', '428', '435', '436', '441', '444', '453', '456', '458', '461', '462', '471', '477', '480', '481', '486', '493']

[11]:

better_models = pd.concat(

[model_losses_df.mean(axis=0), model_losses_df.mean(axis=0)], axis=1

)

better_models.columns = pd.Index(["Same or worse", "Better"])

better = better_models.index.isin(stepm.superior_models)

worse = np.logical_not(better)

better_models.loc[better, "Same or worse"] = np.nan

better_models.loc[worse, "Better"] = np.nan

fig = better_models.plot(style=["o", "s"], rot=270)

The Model Confidence Set¶

The model confidence set takes a set of losses as its input and finds the set which are not statistically different from each other while controlling the familywise error rate. The primary output is a set of p-values, where models with a pvalue above the size are in the MCS. Small p-values indicate that the model is easily rejected from the set that includes the best.

[12]:

from arch.bootstrap import MCS

# Limit the size of the set

losses = model_losses_df.iloc[:, ::20]

mcs = MCS(losses, size=0.10)

mcs.compute()

print("MCS P-values")

print(mcs.pvalues)

print("Included")

included = mcs.included

print([model.split(".")[1] for model in included])

print("Excluded")

excluded = mcs.excluded

print([model.split(".")[1] for model in excluded])

MCS P-values

Pvalue

Model name

model.0 0.000

model.200 0.000

model.40 0.000

model.280 0.001

model.20 0.001

model.100 0.003

model.220 0.003

model.160 0.006

model.140 0.026

model.300 0.032

model.240 0.058

model.120 0.116

model.360 0.116

model.180 0.116

model.60 0.133

model.80 0.272

model.320 0.451

model.440 0.561

model.380 0.561

model.260 0.561

model.340 0.561

model.420 0.561

model.460 0.561

model.400 0.561

model.480 1.000

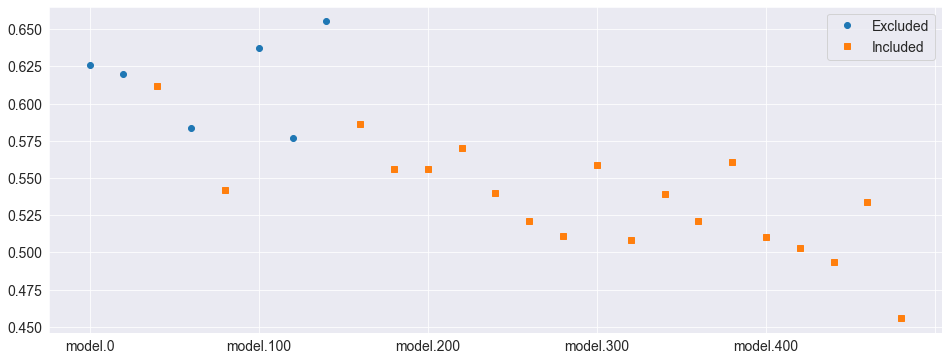

Included

['120', '180', '260', '320', '340', '360', '380', '400', '420', '440', '460', '480', '60', '80']

Excluded

['0', '100', '140', '160', '20', '200', '220', '240', '280', '300', '40']

[13]:

status = pd.DataFrame(

[losses.mean(axis=0), losses.mean(axis=0)], index=["Excluded", "Included"]

).T

status.loc[status.index.isin(included), "Excluded"] = np.nan

status.loc[status.index.isin(excluded), "Included"] = np.nan

fig = status.plot(style=["o", "s"])