Examples¶

System regression simultaneously estimates multiple models. This has three distinct advantages:

Joint inference across models

Linear restrictions can be imposed on the parameters across different models

Improved precision of parameter estimates (depending on the model specification and data)

There are \(K\) models and each model can be expressed in vector notation as

so that the set of models can be expressed as

where \(Y\) is a column vector that stacks the vectors \(Y_i\) for \(i=1,2,\ldots,K\), \(X\) is a block-diagonal matrix where diagonal block i is \(X_i\), \(\beta\) is a stacked vector of the \(K\) \(\beta_i\)s and \(\epsilon\) is similarly comprised of the stacked columns of \(\epsilon_i\).

The model can be estimated using OLS with the usual estimator

Since there are multiple series, a GLS estimator that accounts for the cross-sectional heteroskedasticity as well as the correlation of residuals can be estimated

where \(\Omega^{-1} = \Sigma^{-1} \otimes I_{T}\), \(\Sigma_{ij}\) is the covariance between \(\epsilon_i\) and \(\epsilon_j\) and \(T\) is the number of observations. The GLS estimator is only beneficial when the regressors in different models differ and when residuals are correlated. There GLS estimates are identical to the multivariate OLS estimates when all regressors are common.

[1]:

# Common libraries

import numpy as np

import pandas as pd

import seaborn as sns

import statsmodels.api as sm

Data¶

Two data sets will be used. The first is from Munnell which looks at the effect of capital on state GDP. This example follows the example in Chapter 10 in recent editions of Greene”s Econometric Analysis.

The data is state-level but the model is estimated in region. The first step is to aggregate the data by region. All capital measures are summed and the unemployment rate is averaged using weights proportional to the total employment in each state.

[2]:

from linearmodels.datasets import munnell

data = munnell.load()

regions = {

"GF": ["AL", "FL", "LA", "MS"],

"MW": ["IL", "IN", "KY", "MI", "MN", "OH", "WI"],

"MA": ["DE", "MD", "NJ", "NY", "PA", "VA"],

"MT": ["CO", "ID", "MT", "ND", "SD", "WY"],

"NE": ["CT", "ME", "MA", "NH", "RI", "VT"],

"SO": ["GA", "NC", "SC", "TN", "WV", "AR"],

"SW": ["AZ", "NV", "NM", "TX", "UT"],

"CN": ["AK", "IA", "KS", "MO", "NE", "OK"],

"WC": ["CA", "OR", "WA"],

}

def map_region(state):

for key in regions:

if state in regions[key]:

return key

data["REGION"] = data.ST_ABB.map(map_region)

data["TOTAL_EMP"] = data.groupby(["REGION", "YR"])["EMP"].transform("sum")

data["EMP_SHARE"] = data.EMP / data.TOTAL_EMP

data["WEIGHED_UNEMP"] = data.EMP_SHARE * data.UNEMP

A groupby transformation is used to aggregate the data, and finally all values except the unemployment rate are logged.

[3]:

grouped = data.groupby(["REGION", "YR"])

agg_data = grouped[["GSP", "PC", "HWY", "WATER", "UTIL", "EMP", "WEIGHED_UNEMP"]].sum()

for col in ["GSP", "PC", "HWY", "WATER", "UTIL", "EMP"]:

agg_data["ln" + col] = np.log(agg_data[col])

agg_data["UNEMP"] = agg_data.WEIGHED_UNEMP

agg_data["Intercept"] = 1.0

Basic Usage¶

Seemingly Unrelated Models are fairly complex and each equation could have a different number of regressors. As a result, it is not possibly to use standard pandas or numpy data structures, and so dictionaries (or technically dictionary-like objects) are used. In practice, it is strongly recommended to use a OrderedDictionary from the collections module. This ensures that equation order will be preserved. In addition, the dictionary must have the following structure:

keysmust be strings and will be used as equation labelsThe value associated with each key must be either a dictionary or a tuple.

When a dictionary is used, it must have two keys,

dependentandexog. It can optionally have a third keyweightswhich provides weights to use in the regression.When a tuple is used, it must have two elements and takes the form

(dependent, exog). It can optionally contains weights in which case it takes the form(dependent, exog, weights).

This example uses the dictionary syntax to contain the data for each region and uses the region identified as the equation label.

[4]:

from collections import OrderedDict

mod_data = OrderedDict()

for region in ["GF", "SW", "WC", "MT", "NE", "MA", "SO", "MW", "CN"]:

region_data = agg_data.loc[region]

dependent = region_data.lnGSP

exog = region_data[

["Intercept", "lnPC", "lnHWY", "lnWATER", "lnUTIL", "lnEMP", "UNEMP"]

]

mod_data[region] = {"dependent": dependent, "exog": exog}

Fitting the model is virtually identical to fitting any other model with the exception of the special data structure required.

The fitting options here ensure that the homoskedastic covariance estimator are used (cov_type="unadjusted") and that a small sample adjustment is applied. By default, GLS is used (this can be overridden using method="ols".

[5]:

from linearmodels.system import SUR

mod = SUR(mod_data)

res = mod.fit(cov_type="unadjusted")

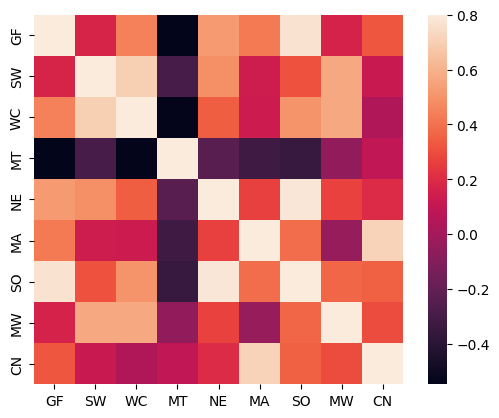

One of the requirements for there to be an efficiency gain in a SUR is that the residuals are correlated. A heatmap is used to inspect this correlation, which is substantial and varies by region.

[6]:

import matplotlib.pyplot as plt

cov = res.sigma

std = np.sqrt(np.diag(res.sigma)[:, None])

regions = list(mod_data.keys())

corr = pd.DataFrame(cov / (std @ std.T), columns=regions, index=regions)

sns.heatmap(corr, vmax=0.8, square=True)

plt.show()

corr.style.format("{:0.3f}")

[6]:

| GF | SW | WC | MT | NE | MA | SO | MW | CN | |

|---|---|---|---|---|---|---|---|---|---|

| GF | 1.000 | 0.173 | 0.447 | -0.547 | 0.525 | 0.425 | 0.763 | 0.167 | 0.325 |

| SW | 0.173 | 1.000 | 0.697 | -0.290 | 0.489 | 0.132 | 0.314 | 0.565 | 0.119 |

| WC | 0.447 | 0.697 | 1.000 | -0.537 | 0.343 | 0.130 | 0.505 | 0.574 | 0.037 |

| MT | -0.547 | -0.290 | -0.537 | 1.000 | -0.241 | -0.322 | -0.351 | -0.058 | 0.091 |

| NE | 0.525 | 0.489 | 0.343 | -0.241 | 1.000 | 0.259 | 0.783 | 0.269 | 0.200 |

| MA | 0.425 | 0.132 | 0.130 | -0.322 | 0.259 | 1.000 | 0.388 | -0.037 | 0.713 |

| SO | 0.763 | 0.314 | 0.505 | -0.351 | 0.783 | 0.388 | 1.000 | 0.366 | 0.350 |

| MW | 0.167 | 0.565 | 0.574 | -0.058 | 0.269 | -0.037 | 0.366 | 1.000 | 0.298 |

| CN | 0.325 | 0.119 | 0.037 | 0.091 | 0.200 | 0.713 | 0.350 | 0.298 | 1.000 |

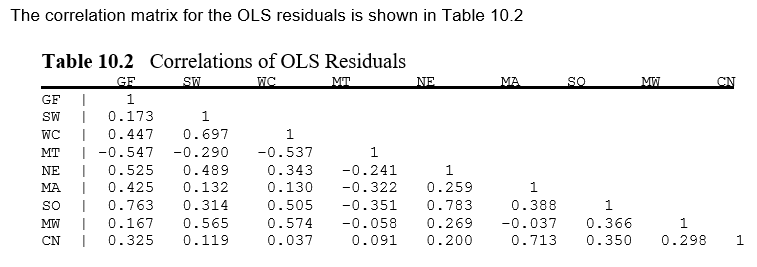

These values can be seen to be identical to the reported results in the existing example from Greene.

[7]:

from IPython.display import Image, display_png

display_png(Image("system_correct-greene-table-10-2.png"))

The full result is fairly long and so here I only print the first 33 lines which show results for two regions. By default it reports all estimates along with the usual measures of precision.

[8]:

print("\n".join(res.summary.as_text().split("\n")[:33]))

System GLS Estimation Summary

===================================================================================

Estimator: GLS Overall R-squared: 0.9937

No. Equations.: 9 McElroy's R-squared: 0.9988

No. Observations: 17 Judge's (OLS) R-squared: 0.9937

Date: Tue, Oct 21 2025 Berndt's R-squared: 1.0000

Time: 13:37:41 Dhrymes's R-squared: 0.9937

Cov. Estimator: unadjusted

Num. Constraints: None

Equation: GF, Dependent Variable: lnGSP

==============================================================================

Parameter Std. Err. T-stat P-value Lower CI Upper CI

------------------------------------------------------------------------------

Intercept 12.310 2.2513 5.4680 0.0000 7.8976 16.723

lnPC -0.2010 0.1424 -1.4117 0.1580 -0.4800 0.0780

lnHWY -1.8856 0.5169 -3.6480 0.0003 -2.8987 -0.8725

lnWATER 0.1785 0.0607 2.9399 0.0033 0.0595 0.2975

lnUTIL 1.1898 0.3744 3.1774 0.0015 0.4559 1.9237

lnEMP 0.9533 0.0847 11.252 0.0000 0.7872 1.1193

UNEMP -0.0031 0.0021 -1.5007 0.1334 -0.0072 0.0009

Equation: SW, Dependent Variable: lnGSP

==============================================================================

Parameter Std. Err. T-stat P-value Lower CI Upper CI

------------------------------------------------------------------------------

Intercept 4.0831 0.9979 4.0918 0.0000 2.1273 6.0389

lnPC 0.0766 0.0858 0.8929 0.3719 -0.0916 0.2449

lnHWY -0.1312 0.1279 -1.0258 0.3050 -0.3819 0.1195

lnWATER -0.1360 0.0611 -2.2240 0.0261 -0.2558 -0.0161

lnUTIL 0.5216 0.1107 4.7102 0.0000 0.3045 0.7386

lnEMP 0.5387 0.0849 6.3439 0.0000 0.3723 0.7051

UNEMP -0.0156 0.0025 -6.2950 0.0000 -0.0205 -0.0108

Equation: WC, Dependent Variable: lnGSP

==============================================================================

Individual results are contained in a dictionary located at the attribute equations and can be accessed using equation labels (available using the attribute equation_labels). Additional information about the model is presented in this view. The West Coast results are show.

[9]:

print(res.equations["WC"])

GLS Estimation Summary

==============================================================================

Eq. Label: WC R-squared: 0.9937

Dep. Variable: lnGSP Adj. R-squared: 0.9900

Estimator: GLS Cov. Estimator: unadjusted

No. Observations: 17 F-statistic: 2862.4

Date: Tue, Oct 21 2025 P-value (F-stat) 0.0000

Time: 13:37:41 Distribution: chi2(6)

Parameter Estimates

==============================================================================

Parameter Std. Err. T-stat P-value Lower CI Upper CI

------------------------------------------------------------------------------

Intercept 1.9602 3.4542 0.5675 0.5704 -4.8100 8.7303

lnPC 0.1699 0.0919 1.8500 0.0643 -0.0101 0.3500

lnHWY 0.1317 0.1138 1.1569 0.2473 -0.0914 0.3547

lnWATER -0.3470 0.1733 -2.0020 0.0453 -0.6867 -0.0073

lnUTIL 0.0895 0.4642 0.1928 0.8471 -0.8204 0.9994

lnEMP 1.0696 0.1708 6.2634 0.0000 0.7349 1.4043

UNEMP -0.0060 0.0042 -1.4180 0.1562 -0.0143 0.0023

==============================================================================

Covariance Estimator:

Homoskedastic (Unadjusted) Covariance (Debiased: False, GLS: True)

The current version of the model does not facilitate cross equation comparisons and so this is manually implemented here.

[10]:

# TODO: Implement method to compare across equations

params = [res.equations[label].params for label in res.equation_labels]

params = pd.concat(params, axis=1)

params.columns = res.equation_labels

params.T.style.format("{:0.3f}")

[10]:

| Intercept | lnPC | lnHWY | lnWATER | lnUTIL | lnEMP | UNEMP | |

|---|---|---|---|---|---|---|---|

| GF | 12.310 | -0.201 | -1.886 | 0.178 | 1.190 | 0.953 | -0.003 |

| SW | 4.083 | 0.077 | -0.131 | -0.136 | 0.522 | 0.539 | -0.016 |

| WC | 1.960 | 0.170 | 0.132 | -0.347 | 0.090 | 1.070 | -0.006 |

| MT | 3.463 | -0.115 | 0.180 | 0.262 | -0.330 | 1.079 | -0.001 |

| NE | -12.294 | 0.118 | 0.934 | -0.557 | -0.290 | 2.494 | 0.020 |

| MA | -18.616 | -0.311 | 3.060 | -0.109 | -1.659 | 2.186 | 0.018 |

| SO | 3.162 | -0.063 | -0.641 | -0.081 | 0.281 | 1.620 | 0.008 |

| MW | -9.258 | 0.096 | 1.612 | 0.694 | -0.340 | -0.062 | -0.031 |

| CN | -3.405 | 0.295 | 0.934 | 0.539 | 0.003 | -0.321 | -0.029 |

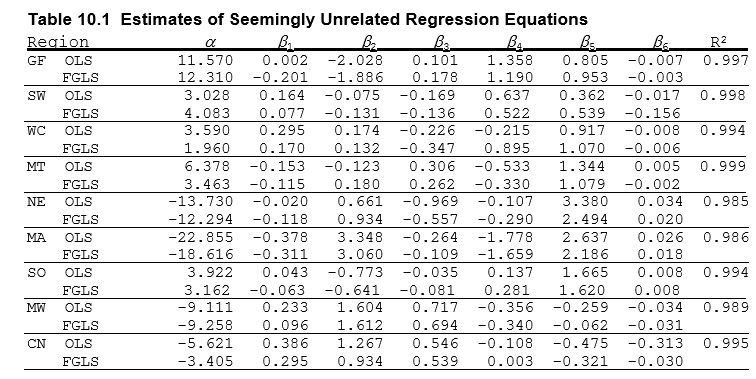

These results can be compared to the results in Greene – they are unsurprisingly identical.

[11]:

display_png(Image("system_correct-greene-table-10-1.png"))

The GLS estimation method requires stronger assumptions for parameter estimates to be consistent. If these are violated then it might be the case that OLS is still consistent (in some sense) and so OLS can be used by passing method="ols" when calling fit.

These results can be compared to Greene”s table – they are identical except the final value which seems to have a small typo.

[12]:

res_ols = mod.fit(method="ols", debiased=True, cov_type="unadjusted")

params = []

r2 = []

for label in res.equation_labels:

params.append(res_ols.equations[label].params)

r2.append(res_ols.equations[label].rsquared)

params = pd.concat(params, axis=1)

params.columns = res.equation_labels

params = params.T

params["R2"] = r2

params.style.format("{:0.3f}")

[12]:

| Intercept | lnPC | lnHWY | lnWATER | lnUTIL | lnEMP | UNEMP | R2 | |

|---|---|---|---|---|---|---|---|---|

| GF | 11.567 | 0.002 | -2.029 | 0.101 | 1.358 | 0.805 | -0.007 | 0.997 |

| SW | 3.028 | 0.164 | -0.075 | -0.169 | 0.637 | 0.362 | -0.017 | 0.998 |

| WC | 3.590 | 0.295 | 0.174 | -0.226 | -0.214 | 0.917 | -0.008 | 0.994 |

| MT | 6.378 | -0.153 | -0.123 | 0.306 | -0.533 | 1.344 | 0.005 | 0.999 |

| NE | -13.730 | -0.020 | 0.662 | -0.969 | -0.107 | 3.380 | 0.034 | 0.985 |

| MA | -22.855 | -0.378 | 3.348 | -0.264 | -1.778 | 2.673 | 0.026 | 0.986 |

| SO | 3.927 | 0.043 | -0.773 | -0.035 | 0.140 | 1.665 | 0.008 | 0.994 |

| MW | -9.111 | 0.233 | 1.604 | 0.717 | -0.356 | -0.259 | -0.034 | 0.989 |

| CN | -5.621 | 0.386 | 1.267 | 0.546 | -0.108 | -0.475 | -0.031 | 0.995 |

The parameter estimates for one coefficient – unemployment – can be compared across the two estimation methods.

[13]:

params = pd.concat(

[

res_ols.params.iloc[1::7],

res_ols.std_errors.iloc[1::7],

res.params.iloc[1::7],

res.std_errors.iloc[1::7],

],

axis=1,

)

params.columns = ["OLS", "OLS se", "GLS", "GLS se"]

params.index = regions

params

[13]:

| OLS | OLS se | GLS | GLS se | |

|---|---|---|---|---|

| GF | 0.002124 | 0.301235 | -0.200966 | 0.142355 |

| SW | 0.163546 | 0.165995 | 0.076637 | 0.085831 |

| WC | 0.294855 | 0.205417 | 0.169950 | 0.091865 |

| MT | -0.152601 | 0.084031 | -0.114834 | 0.048489 |

| NE | -0.020407 | 0.285621 | 0.118316 | 0.131329 |

| MA | -0.377570 | 0.167307 | -0.310861 | 0.080893 |

| SO | 0.042818 | 0.279472 | -0.063212 | 0.104344 |

| MW | 0.233403 | 0.206248 | 0.095886 | 0.101564 |

| CN | 0.385885 | 0.211083 | 0.294570 | 0.090104 |

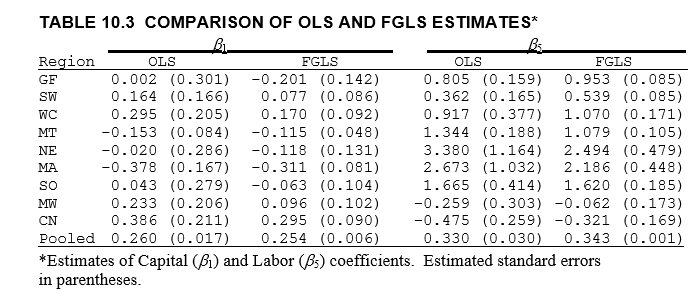

The parameters and their standard errors match those reported in Greene.

[14]:

display_png(Image("system_correct-greene-table-10-3.png"))

Estimation Options¶

Iterative GLS¶

These next examples use data on fringe benefits from F. Vella (1993), “A Simple Estimator for Simultaneous Models with Censored Endogenous Regressors” which appears in Wooldridge (2002). The model consists of two equations, one for hourly wage and the other for hourly benefits. The initial model uses the same regressors in both equations.

[15]:

from linearmodels.datasets import fringe

print(fringe.DESCR)

fdata = fringe.load()

F. Vella (1993), "A Simple Estimator for Simultaneous Models with Censored

Endogenous Regressors," International Economic Review 34, 441-457.

annearn annual earnings, $

hrearn hourly earnings, $

exper years work experience

age age in years

depends number of dependents

married =1 if married

tenure years with current employer

educ years schooling

nrtheast =1 if live in northeast

nrthcen =1 if live in north central

south =1 if live in south

male =1 if male

white =1 if white

union =1 if union member

office =1 if office worker

annhrs annual hours worked

ind1 =1 if industry == 1

ind2 =1 if industry == 2

ind3 =1 if industry == 3

ind4 =1 if industry == 4

ind5 =1 if industry == 5

ind6 =1 if industry == 6

ind7 =1 if industry == 7

ind8 =1 if industry == 8

ind9 =1 if industry == 9

vacdays $ value of vac days

sicklve $ value of sick leave

insur $ value of employee insur

pension $ value of employee pension

annbens vacdays+sicklve+insur+pension

hrbens hourly benefits, $

annhrssq annhrs^2

beratio annbens/annearn

lannhrs log(annhrs)

tenuresq tenure^2

expersq exper^2

lannearn log(annearn)

peratio pension/annearn

vserat (vacdays+sicklve)/annearn

The estimated model is reported as “System OLS Estimation” since when all regressors are identical, OLS is used since GLS brings no efficiency gains. OLS will be used when the data structure containing the exogenous regressors in each equations is the same (i.e., id(exog) is the same for all equations).

[16]:

exog = sm.add_constant(

fdata[

[

"educ",

"exper",

"expersq",

"tenure",

"tenuresq",

"union",

"south",

"nrtheast",

"nrthcen",

"married",

"white",

"male",

]

]

)

fmod_data = OrderedDict()

fmod_data["hrearn"] = {"dependent": fdata.hrearn, "exog": exog}

fmod_data["hrbens"] = {"dependent": fdata.hrbens, "exog": exog}

fmod = SUR(fmod_data)

print(fmod.fit(cov_type="unadjusted"))

System OLS Estimation Summary

===================================================================================

Estimator: OLS Overall R-squared: 0.2087

No. Equations.: 2 McElroy's R-squared: 0.2926

No. Observations: 616 Judge's (OLS) R-squared: 0.2087

Date: Tue, Oct 21 2025 Berndt's R-squared: 0.4822

Time: 13:37:42 Dhrymes's R-squared: 0.2087

Cov. Estimator: unadjusted

Num. Constraints: None

Equation: hrearn, Dependent Variable: hrearn

==============================================================================

Parameter Std. Err. T-stat P-value Lower CI Upper CI

------------------------------------------------------------------------------

const -2.6321 1.2153 -2.1658 0.0303 -5.0141 -0.2502

educ 0.4588 0.0684 6.7085 0.0000 0.3248 0.5929

exper -0.0758 0.0567 -1.3367 0.1813 -0.1870 0.0354

expersq 0.0040 0.0012 3.4274 0.0006 0.0017 0.0063

tenure 0.1101 0.0829 1.3276 0.1843 -0.0524 0.2726

tenuresq -0.0051 0.0032 -1.5640 0.1178 -0.0114 0.0013

union 0.8080 0.4035 2.0026 0.0452 0.0172 1.5988

south -0.4566 0.5459 -0.8365 0.4029 -1.5265 0.6132

nrtheast -1.1508 0.5993 -1.9201 0.0548 -2.3254 0.0239

nrthcen -0.6363 0.5501 -1.1565 0.2475 -1.7145 0.4420

married 0.6424 0.4134 1.5540 0.1202 -0.1678 1.4526

white 1.1409 0.6054 1.8844 0.0595 -0.0458 2.3275

male 1.7847 0.3938 4.5322 0.0000 1.0129 2.5565

Equation: hrbens, Dependent Variable: hrbens

==============================================================================

Parameter Std. Err. T-stat P-value Lower CI Upper CI

------------------------------------------------------------------------------

const -0.8897 0.1453 -6.1225 0.0000 -1.1746 -0.6049

educ 0.0768 0.0082 9.3896 0.0000 0.0608 0.0928

exper 0.0226 0.0068 3.3259 0.0009 0.0093 0.0359

expersq -0.0005 0.0001 -3.3965 0.0007 -0.0007 -0.0002

tenure 0.0536 0.0099 5.4011 0.0000 0.0341 0.0730

tenuresq -0.0012 0.0004 -3.0014 0.0027 -0.0019 -0.0004

union 0.3659 0.0482 7.5839 0.0000 0.2713 0.4605

south -0.0227 0.0653 -0.3476 0.7282 -0.1506 0.1052

nrtheast -0.0567 0.0717 -0.7918 0.4285 -0.1972 0.0837

nrthcen -0.0380 0.0658 -0.5776 0.5635 -0.1669 0.0909

married 0.0579 0.0494 1.1706 0.2418 -0.0390 0.1547

white 0.0902 0.0724 1.2453 0.2130 -0.0517 0.2321

male 0.2683 0.0471 5.6985 0.0000 0.1760 0.3606

==============================================================================

Covariance Estimator:

Homoskedastic (Unadjusted) Covariance (Debiased: False, GLS: False)

The estimator can be forced to use GLS by setting method="gls". As can be seen below, the parameter estimates and standard errors do not change even though two-stage GLS is used. The \(R^2\) does change since the left-hand side variable is transformed by the GLS weighting before estimation.

[17]:

print(fmod.fit(method="gls", cov_type="unadjusted"))

System GLS Estimation Summary

===================================================================================

Estimator: GLS Overall R-squared: 0.2087

No. Equations.: 2 McElroy's R-squared: 0.2926

No. Observations: 616 Judge's (OLS) R-squared: 0.2087

Date: Tue, Oct 21 2025 Berndt's R-squared: 0.4822

Time: 13:37:42 Dhrymes's R-squared: 0.2087

Cov. Estimator: unadjusted

Num. Constraints: None

Equation: hrearn, Dependent Variable: hrearn

==============================================================================

Parameter Std. Err. T-stat P-value Lower CI Upper CI

------------------------------------------------------------------------------

const -2.6321 1.2153 -2.1658 0.0303 -5.0141 -0.2502

educ 0.4588 0.0684 6.7085 0.0000 0.3248 0.5929

exper -0.0758 0.0567 -1.3367 0.1813 -0.1870 0.0354

expersq 0.0040 0.0012 3.4274 0.0006 0.0017 0.0063

tenure 0.1101 0.0829 1.3276 0.1843 -0.0524 0.2726

tenuresq -0.0051 0.0032 -1.5640 0.1178 -0.0114 0.0013

union 0.8080 0.4035 2.0026 0.0452 0.0172 1.5988

south -0.4566 0.5459 -0.8365 0.4029 -1.5265 0.6132

nrtheast -1.1508 0.5993 -1.9201 0.0548 -2.3254 0.0239

nrthcen -0.6363 0.5501 -1.1565 0.2475 -1.7145 0.4420

married 0.6424 0.4134 1.5540 0.1202 -0.1678 1.4526

white 1.1409 0.6054 1.8844 0.0595 -0.0458 2.3275

male 1.7847 0.3938 4.5322 0.0000 1.0129 2.5565

Equation: hrbens, Dependent Variable: hrbens

==============================================================================

Parameter Std. Err. T-stat P-value Lower CI Upper CI

------------------------------------------------------------------------------

const -0.8897 0.1453 -6.1225 0.0000 -1.1746 -0.6049

educ 0.0768 0.0082 9.3896 0.0000 0.0608 0.0928

exper 0.0226 0.0068 3.3259 0.0009 0.0093 0.0359

expersq -0.0005 0.0001 -3.3965 0.0007 -0.0007 -0.0002

tenure 0.0536 0.0099 5.4011 0.0000 0.0341 0.0730

tenuresq -0.0012 0.0004 -3.0014 0.0027 -0.0019 -0.0004

union 0.3659 0.0482 7.5839 0.0000 0.2713 0.4605

south -0.0227 0.0653 -0.3476 0.7282 -0.1506 0.1052

nrtheast -0.0567 0.0717 -0.7918 0.4285 -0.1972 0.0837

nrthcen -0.0380 0.0658 -0.5776 0.5635 -0.1669 0.0909

married 0.0579 0.0494 1.1706 0.2418 -0.0390 0.1547

white 0.0902 0.0724 1.2453 0.2130 -0.0517 0.2321

male 0.2683 0.0471 5.6985 0.0000 0.1760 0.3606

==============================================================================

Covariance Estimator:

Homoskedastic (Unadjusted) Covariance (Debiased: False, GLS: True)

The regressors must differ in order to see gains to GLS. Here insignificant variables are dropped from each equation so that the regressors will no longer be identical. The typical standard error is marginally smaller, although this might be due to dropping regressors.

[18]:

exog_earn = sm.add_constant(

fdata[["educ", "exper", "expersq", "union", "nrtheast", "white"]]

)

exog_bens = sm.add_constant(

fdata[["educ", "exper", "expersq", "tenure", "tenuresq", "union", "male"]]

)

fmod_data["hrearn"] = {"dependent": fdata.hrearn, "exog": exog_earn}

fmod_data["hrbens"] = {"dependent": fdata.hrbens, "exog": exog_bens}

fmod = SUR(fmod_data)

print(fmod.fit(cov_type="unadjusted"))

System GLS Estimation Summary

===================================================================================

Estimator: GLS Overall R-squared: 0.1685

No. Equations.: 2 McElroy's R-squared: 0.2762

No. Observations: 616 Judge's (OLS) R-squared: 0.1685

Date: Tue, Oct 21 2025 Berndt's R-squared: 0.4504

Time: 13:37:42 Dhrymes's R-squared: 0.1685

Cov. Estimator: unadjusted

Num. Constraints: None

Equation: hrearn, Dependent Variable: hrearn

==============================================================================

Parameter Std. Err. T-stat P-value Lower CI Upper CI

------------------------------------------------------------------------------

const -2.5240 1.0857 -2.3246 0.0201 -4.6520 -0.3959

educ 0.5000 0.0685 7.2987 0.0000 0.3657 0.6342

exper -0.0212 0.0522 -0.4058 0.6849 -0.1234 0.0811

expersq 0.0032 0.0011 2.8776 0.0040 0.0010 0.0055

union 1.1043 0.3928 2.8116 0.0049 0.3345 1.8741

nrtheast -0.5343 0.4305 -1.2411 0.2146 -1.3780 0.3095

white 1.1320 0.5845 1.9368 0.0528 -0.0136 2.2776

Equation: hrbens, Dependent Variable: hrbens

==============================================================================

Parameter Std. Err. T-stat P-value Lower CI Upper CI

------------------------------------------------------------------------------

const -0.8231 0.1176 -7.0021 0.0000 -1.0535 -0.5927

educ 0.0791 0.0080 9.8927 0.0000 0.0634 0.0948

exper 0.0260 0.0066 3.9114 0.0001 0.0130 0.0390

expersq -0.0005 0.0001 -3.8469 0.0001 -0.0008 -0.0003

tenure 0.0494 0.0094 5.2409 0.0000 0.0309 0.0679

tenuresq -0.0010 0.0004 -2.6275 0.0086 -0.0017 -0.0002

union 0.3766 0.0475 7.9259 0.0000 0.2835 0.4698

male 0.2141 0.0433 4.9413 0.0000 0.1292 0.2990

==============================================================================

Covariance Estimator:

Homoskedastic (Unadjusted) Covariance (Debiased: False, GLS: True)

The standard method to estimate models uses two steps. The first uses OLS to estimate the parameters so that the residual covariance can be estimated. The second stage uses the estimated covariance to estimate the model via GLS. Iterative GLS can be used to continue these iterations using the most recent step to estimate the residual covariance and then re-estimating the parameters using GLS. This option can be used by setting iterate=True.

[19]:

fmod_res = fmod.fit(cov_type="unadjusted", iterate=True)

print(fmod_res)

System Iterative GLS Estimation Summary

===================================================================================

Estimator: Iterative GLS Overall R-squared: 0.1685

No. Equations.: 2 McElroy's R-squared: 0.2749

No. Observations: 616 Judge's (OLS) R-squared: 0.1685

Date: Tue, Oct 21 2025 Berndt's R-squared: 0.4532

Time: 13:37:42 Dhrymes's R-squared: 0.1685

Cov. Estimator: unadjusted

Num. Constraints: None

Equation: hrearn, Dependent Variable: hrearn

==============================================================================

Parameter Std. Err. T-stat P-value Lower CI Upper CI

------------------------------------------------------------------------------

const -2.5147 1.0858 -2.3161 0.0206 -4.6428 -0.3867

educ 0.5001 0.0685 7.3004 0.0000 0.3658 0.6344

exper -0.0211 0.0522 -0.4044 0.6859 -0.1233 0.0811

expersq 0.0032 0.0011 2.8760 0.0040 0.0010 0.0055

union 1.1043 0.3928 2.8115 0.0049 0.3345 1.8741

nrtheast -0.5314 0.4305 -1.2342 0.2171 -1.3752 0.3124

white 1.1191 0.5845 1.9145 0.0556 -0.0266 2.2648

Equation: hrbens, Dependent Variable: hrbens

==============================================================================

Parameter Std. Err. T-stat P-value Lower CI Upper CI

------------------------------------------------------------------------------

const -0.8223 0.1176 -6.9947 0.0000 -1.0527 -0.5919

educ 0.0792 0.0080 9.9004 0.0000 0.0635 0.0948

exper 0.0260 0.0066 3.9213 0.0001 0.0130 0.0390

expersq -0.0005 0.0001 -3.8528 0.0001 -0.0008 -0.0003

tenure 0.0492 0.0094 5.2189 0.0000 0.0307 0.0677

tenuresq -0.0010 0.0004 -2.6025 0.0093 -0.0017 -0.0002

union 0.3771 0.0475 7.9364 0.0000 0.2840 0.4703

male 0.2107 0.0433 4.8627 0.0000 0.1258 0.2956

==============================================================================

Covariance Estimator:

Homoskedastic (Unadjusted) Covariance (Debiased: False, GLS: True)

The number of GLS iterations can be verified using the iterations attribute of the results.

[20]:

fmod_res.iterations

[20]:

5

Alternative Covariance Estimators¶

The estimator supports heteroskedasticity robust covariance estimation b setting cov_type="robust". The estimator allows for arbitrary correlation across series with the same time index but not correlation across time periods, which is the same assumption as in the unadjusted estimator. The main difference is that this estimator will correct standard errors for dependence between regressors (or squared regressors) and squared residuals.

Heteroskedasticity Robust Covariance Estimation¶

In the fringe benefit model there are some large differences between standard errors computed using the the homoskedastic covariance estimator and the heteroskedasticity robust covariance estimator (e.g., exper).

[21]:

fres_het = fmod.fit(cov_type="robust")

print(fres_het.summary)

System GLS Estimation Summary

===================================================================================

Estimator: GLS Overall R-squared: 0.1685

No. Equations.: 2 McElroy's R-squared: 0.2762

No. Observations: 616 Judge's (OLS) R-squared: 0.1685

Date: Tue, Oct 21 2025 Berndt's R-squared: 0.4504

Time: 13:37:42 Dhrymes's R-squared: 0.1685

Cov. Estimator: robust

Num. Constraints: None

Equation: hrearn, Dependent Variable: hrearn

==============================================================================

Parameter Std. Err. T-stat P-value Lower CI Upper CI

------------------------------------------------------------------------------

const -2.5240 0.8703 -2.9002 0.0037 -4.2297 -0.8183

educ 0.5000 0.0809 6.1765 0.0000 0.3413 0.6586

exper -0.0212 0.2270 -0.0932 0.9257 -0.4661 0.4237

expersq 0.0032 0.0059 0.5507 0.5819 -0.0083 0.0148

union 1.1043 0.2857 3.8647 0.0001 0.5443 1.6644

nrtheast -0.5343 0.5273 -1.0132 0.3110 -1.5678 0.4992

white 1.1320 0.4921 2.3002 0.0214 0.1674 2.0966

Equation: hrbens, Dependent Variable: hrbens

==============================================================================

Parameter Std. Err. T-stat P-value Lower CI Upper CI

------------------------------------------------------------------------------

const -0.8231 0.1082 -7.6087 0.0000 -1.0352 -0.6111

educ 0.0791 0.0081 9.7768 0.0000 0.0632 0.0949

exper 0.0260 0.0059 4.3675 0.0000 0.0143 0.0376

expersq -0.0005 0.0001 -4.2494 0.0000 -0.0008 -0.0003

tenure 0.0494 0.0097 5.0775 0.0000 0.0303 0.0685

tenuresq -0.0010 0.0004 -2.4121 0.0159 -0.0018 -0.0002

union 0.3766 0.0514 7.3342 0.0000 0.2760 0.4773

male 0.2141 0.0397 5.3975 0.0000 0.1363 0.2918

==============================================================================

Covariance Estimator:

Heteroskedastic (Robust) Covariance (Debiased: False, GLS: True)

Other supported covariance estimators include "kernel” which implements a HAC and "clustered" which supports 1 and 2-way clustering.

Kernel (HAC)¶

The supported kernels are "bartlett" (Newey-West), "parzen" (Gallant), and qs (Quadratic Spectral, Andrews). This example uses the Parzen kernel. The kernel’s bandwidth is computed automatically if the parameter bandwidth is not provided.

[22]:

hac_res = fmod.fit(cov_type="kernel", kernel="parzen")

print(hac_res.summary)

System GLS Estimation Summary

===================================================================================

Estimator: GLS Overall R-squared: 0.1685

No. Equations.: 2 McElroy's R-squared: 0.2762

No. Observations: 616 Judge's (OLS) R-squared: 0.1685

Date: Tue, Oct 21 2025 Berndt's R-squared: 0.4504

Time: 13:37:42 Dhrymes's R-squared: 0.1685

Cov. Estimator: kernel

Num. Constraints: None

Equation: hrearn, Dependent Variable: hrearn

==============================================================================

Parameter Std. Err. T-stat P-value Lower CI Upper CI

------------------------------------------------------------------------------

const -2.5240 1.0048 -2.5120 0.0120 -4.4933 -0.5547

educ 0.5000 0.0973 5.1391 0.0000 0.3093 0.6907

exper -0.0212 0.2287 -0.0925 0.9263 -0.4694 0.4270

expersq 0.0032 0.0059 0.5486 0.5833 -0.0084 0.0148

union 1.1043 0.2637 4.1882 0.0000 0.5875 1.6211

nrtheast -0.5343 0.4800 -1.1131 0.2657 -1.4750 0.4065

white 1.1320 0.4813 2.3520 0.0187 0.1887 2.0753

Equation: hrbens, Dependent Variable: hrbens

==============================================================================

Parameter Std. Err. T-stat P-value Lower CI Upper CI

------------------------------------------------------------------------------

const -0.8231 0.1344 -6.1228 0.0000 -1.0866 -0.5596

educ 0.0791 0.0095 8.3675 0.0000 0.0606 0.0976

exper 0.0260 0.0064 4.0357 0.0001 0.0134 0.0386

expersq -0.0005 0.0001 -3.9026 0.0001 -0.0008 -0.0003

tenure 0.0494 0.0090 5.5160 0.0000 0.0318 0.0669

tenuresq -0.0010 0.0003 -2.9161 0.0035 -0.0016 -0.0003

union 0.3766 0.0705 5.3407 0.0000 0.2384 0.5148

male 0.2141 0.0577 3.7117 0.0002 0.1010 0.3271

==============================================================================

Covariance Estimator:

Kernel (HAC) Covariance (Debiased: False, GLS: True, Kernel: parzen)

Clustered (Rogers)¶

The clustered covariance estimator requires the clusters to be entered as a NumPy array with shape (nobs, 1) or (nobs, 2). This example uses random clusters to illustrate the structure of the group id variable.

[23]:

rs = np.random.RandomState([983476381, 28390328, 23829810])

random_clusters = rs.randint(0, 51, size=(616, 1))

clustered_res = fmod.fit(cov_type="clustered", clusters=random_clusters)

print(clustered_res.summary)

System GLS Estimation Summary

===================================================================================

Estimator: GLS Overall R-squared: 0.1685

No. Equations.: 2 McElroy's R-squared: 0.2762

No. Observations: 616 Judge's (OLS) R-squared: 0.1685

Date: Tue, Oct 21 2025 Berndt's R-squared: 0.4504

Time: 13:37:42 Dhrymes's R-squared: 0.1685

Cov. Estimator: clustered

Num. Constraints: None

Equation: hrearn, Dependent Variable: hrearn

==============================================================================

Parameter Std. Err. T-stat P-value Lower CI Upper CI

------------------------------------------------------------------------------

const -2.5240 0.8501 -2.9692 0.0030 -4.1901 -0.8579

educ 0.5000 0.0804 6.2174 0.0000 0.3424 0.6576

exper -0.0212 0.2285 -0.0926 0.9262 -0.4690 0.4267

expersq 0.0032 0.0059 0.5479 0.5837 -0.0084 0.0149

union 1.1043 0.2696 4.0963 0.0000 0.5759 1.6327

nrtheast -0.5343 0.5181 -1.0312 0.3024 -1.5497 0.4812

white 1.1320 0.4701 2.4083 0.0160 0.2107 2.0533

Equation: hrbens, Dependent Variable: hrbens

==============================================================================

Parameter Std. Err. T-stat P-value Lower CI Upper CI

------------------------------------------------------------------------------

const -0.8231 0.1077 -7.6435 0.0000 -1.0342 -0.6121

educ 0.0791 0.0080 9.8547 0.0000 0.0634 0.0948

exper 0.0260 0.0059 4.4288 0.0000 0.0145 0.0375

expersq -0.0005 0.0001 -4.6793 0.0000 -0.0007 -0.0003

tenure 0.0494 0.0105 4.7036 0.0000 0.0288 0.0700

tenuresq -0.0010 0.0004 -2.2777 0.0227 -0.0018 -0.0001

union 0.3766 0.0525 7.1717 0.0000 0.2737 0.4795

male 0.2141 0.0317 6.7496 0.0000 0.1519 0.2762

==============================================================================

Covariance Estimator:

Heteroskedastic (Robust) Covariance (Debiased: False, GLS: True, Number of Grouping Variables: 1, Number of Groups: 51 (Variable 0), Group Debias: False)

Prespecified Residual Covariance Estimators¶

The GLS estimator can be used with a user specified covariance. This example uses a covariance where all correlations are identical (equicorrelation) in the state GDP model. The estimator must be used when constructing the model through the sigma keyword argument.

[24]:

avg_corr = (corr - np.eye(9)).mean().mean() * (81 / 72)

rho = np.ones((9, 9)) * avg_corr + (1 - avg_corr) * np.eye(9)

sigma_pre = rho * (std @ std.T)

mod_pre_sigma = SUR(mod_data, sigma=sigma_pre)

res_pre = mod_pre_sigma.fit(cov_type="unadjusted", debiased=True)

print(res_pre.equations["GF"])

GLS Estimation Summary

==============================================================================

Eq. Label: GF R-squared: 0.9966

Dep. Variable: lnGSP Adj. R-squared: 0.9945

Estimator: GLS Cov. Estimator: unadjusted

No. Observations: 17 F-statistic: 549.95

Date: Tue, Oct 21 2025 P-value (F-stat) 0.0000

Time: 13:37:42 Distribution: F(6,90)

Parameter Estimates

==============================================================================

Parameter Std. Err. T-stat P-value Lower CI Upper CI

------------------------------------------------------------------------------

Intercept 7.9753 4.3819 1.8200 0.0988 -1.7883 17.739

lnPC 0.1011 0.2727 0.3708 0.7185 -0.5065 0.7087

lnHWY -0.9882 1.0313 -0.9582 0.3606 -3.2862 1.3098

lnWATER 0.0791 0.1134 0.6971 0.5016 -0.1736 0.3318

lnUTIL 0.5160 0.7720 0.6685 0.5190 -1.2040 2.2361

lnEMP 0.8494 0.1426 5.9557 0.0001 0.5316 1.1671

UNEMP -0.0057 0.0034 -1.6466 0.1307 -0.0134 0.0020

==============================================================================

Covariance Estimator:

Homoskedastic (Unadjusted) Covariance (Debiased: True, GLS: True)

Diagonal Residual Covariance¶

The default assumption is that there can be arbitrary correlation between series. The model can be estimated assuming no correlation but different variance by setting the keyword argument full_cov=False in the fit method. This is only useful when there are cross-equation parameter restrictions.

Cross-Equation Restrictions¶

One of the more useful features of using a SUR to estimate a system is the ability to impose constraints on parameters across equations. Here only linear constraints of the form

are supported. Linear constraints are entered by passing a DataFrame with the shape number of constraints by number of parameters. The number and name of parameters can be seen by inspecting the param_names attribute of a model. Below are the parameter names from the state GDP model which consist of the equation label, an underscore, and the variable name. This ensures uniqueness.

[25]:

mod.param_names[:14]

[25]:

['GF_Intercept',

'GF_lnPC',

'GF_lnHWY',

'GF_lnWATER',

'GF_lnUTIL',

'GF_lnEMP',

'GF_UNEMP',

'SW_Intercept',

'SW_lnPC',

'SW_lnHWY',

'SW_lnWATER',

'SW_lnUTIL',

'SW_lnEMP',

'SW_UNEMP']

The example of a parameter constraint will enforce a common value of the coefficient of unemployment in all equations. This restriction takes the form

where in all examples i is the first series and j is one of the 8 others. In total there are 8 restrictions.

The construction of the restriction array and the non-zero columns are shown below.

[26]:

r = pd.DataFrame(

columns=mod.param_names,

index=["rest{0}".format(i) for i in range(8)],

dtype=np.float64,

)

r.loc[:, :] = 0.0

r.iloc[:, 6] = -1.0

r.iloc[:, 13::7] = np.eye(8)

print(r.iloc[:, 6::7])

GF_UNEMP SW_UNEMP WC_UNEMP MT_UNEMP NE_UNEMP MA_UNEMP SO_UNEMP \

rest0 -1.0 1.0 0.0 0.0 0.0 0.0 0.0

rest1 -1.0 0.0 1.0 0.0 0.0 0.0 0.0

rest2 -1.0 0.0 0.0 1.0 0.0 0.0 0.0

rest3 -1.0 0.0 0.0 0.0 1.0 0.0 0.0

rest4 -1.0 0.0 0.0 0.0 0.0 1.0 0.0

rest5 -1.0 0.0 0.0 0.0 0.0 0.0 1.0

rest6 -1.0 0.0 0.0 0.0 0.0 0.0 0.0

rest7 -1.0 0.0 0.0 0.0 0.0 0.0 0.0

MW_UNEMP CN_UNEMP

rest0 0.0 0.0

rest1 0.0 0.0

rest2 0.0 0.0

rest3 0.0 0.0

rest4 0.0 0.0

rest5 0.0 0.0

rest6 1.0 0.0

rest7 0.0 1.0

The constraint can be added to an existing model using the add_constraint method. This method requires one input, r and optionally q. if q is not provided, it is set to 0.

Here the constraint is added, the model is estimated, and the parameters for unemployment are displayed. They all have the same value.

[27]:

mod.add_constraints(r)

constrained_res = mod.fit()

constrained_res.params[6::7]

[27]:

GF_UNEMP -0.005801

SW_UNEMP -0.005801

WC_UNEMP -0.005801

MT_UNEMP -0.005801

NE_UNEMP -0.005801

MA_UNEMP -0.005801

SO_UNEMP -0.005801

MW_UNEMP -0.005801

CN_UNEMP -0.005801

Name: params, dtype: float64

Pooling using constraints¶

More complicated constraints can be used to produce interesting models. Using the same idea as the previous set of constraints, a pooled SUR (excluding the constant) is constructed by restricting all coefficients to have the same value. Here the form of the restriction is

so that the restriction is identical to the previous, only applied to all variables excluding the constant.

Here the estimated from the first two equations are shown. All coefficients except the intercept are identical across equations.

Note: When linear constraints are imposed, the parameter covariance matrix will be singular. Caution is needed to ensure test statistics are meaningful.

[28]:

r2 = np.zeros((8 * 6, r.shape[1]))

loc = 0

for i in range(6):

for j in range(8):

r2[loc, i + 1] = -1.0

r2[loc, 7 * (j + 1) + i + 1] = 1.0

loc += 1

r2 = pd.DataFrame(r2, columns=mod.param_names)

mod.reset_constraints()

mod.add_constraints(r2)

pooled_res = mod.fit()

print("\n".join(pooled_res.summary.as_text().split("\n")[:33]))

System GLS Estimation Summary

===================================================================================

Estimator: GLS Overall R-squared: 0.9777

No. Equations.: 9 McElroy's R-squared: 0.9891

No. Observations: 17 Judge's (OLS) R-squared: 0.9777

Date: Tue, Oct 21 2025 Berndt's R-squared: 0.9974

Time: 13:37:42 Dhrymes's R-squared: 0.9777

Cov. Estimator: robust

Num. Constraints: 48

Equation: GF, Dependent Variable: lnGSP

==============================================================================

Parameter Std. Err. T-stat P-value Lower CI Upper CI

------------------------------------------------------------------------------

Intercept 0.2732 0.2159 1.2656 0.2057 -0.1499 0.6963

lnPC 0.3639 0.0205 17.763 0.0000 0.3238 0.4041

lnHWY 0.3103 0.0279 11.141 0.0000 0.2557 0.3649

lnWATER 0.0805 0.0109 7.3615 0.0000 0.0591 0.1020

lnUTIL -0.1733 0.0166 -10.466 0.0000 -0.2057 -0.1408

lnEMP 0.6142 0.0248 24.752 0.0000 0.5655 0.6628

UNEMP -0.0128 0.0006 -22.939 0.0000 -0.0139 -0.0117

Equation: SW, Dependent Variable: lnGSP

==============================================================================

Parameter Std. Err. T-stat P-value Lower CI Upper CI

------------------------------------------------------------------------------

Intercept 0.2869 0.2201 1.3034 0.1924 -0.1445 0.7183

lnPC 0.3639 0.0205 17.763 0.0000 0.3238 0.4041

lnHWY 0.3103 0.0279 11.141 0.0000 0.2557 0.3649

lnWATER 0.0805 0.0109 7.3615 0.0000 0.0591 0.1020

lnUTIL -0.1733 0.0166 -10.466 0.0000 -0.2057 -0.1408

lnEMP 0.6142 0.0248 24.752 0.0000 0.5655 0.6628

UNEMP -0.0128 0.0006 -22.939 0.0000 -0.0139 -0.0117

Equation: WC, Dependent Variable: lnGSP

==============================================================================

Multivariate OLS¶

One final feature worth demonstrating is a simple interface for specifying multivariate OLS models. These models have the same regressors and so it is possible to specify them with two arrays. The first is a \(T\) by \(K\) array of dependent variables where each column contains a dependent variable. The second contains the common exogenous regressors.

This example shows how a CAPM can be estimated as a MV OLS.

[29]:

import statsmodels.api as sm

from linearmodels.datasets import french

data = french.load()

factors = sm.add_constant(data[["MktRF"]])

mv_ols = SUR.multivariate_ls(

data[["S1V1", "S1V3", "S1V5", "S5V1", "S5V3", "S5V5"]], factors

)

mv_ols_res = mv_ols.fit(cov_type="unadjusted")

print(mv_ols_res)

System OLS Estimation Summary

===================================================================================

Estimator: OLS Overall R-squared: 0.6564

No. Equations.: 6 McElroy's R-squared: 0.8776

No. Observations: 819 Judge's (OLS) R-squared: 0.6564

Date: Tue, Oct 21 2025 Berndt's R-squared: 0.9773

Time: 13:37:43 Dhrymes's R-squared: 0.6564

Cov. Estimator: unadjusted

Num. Constraints: None

Equation: S1V1, Dependent Variable: S1V1

==============================================================================

Parameter Std. Err. T-stat P-value Lower CI Upper CI

------------------------------------------------------------------------------

const -0.0020 0.0017 -1.1608 0.2457 -0.0054 0.0014

MktRF 1.3736 0.0403 34.101 0.0000 1.2947 1.4526

Equation: S1V3, Dependent Variable: S1V3

==============================================================================

Parameter Std. Err. T-stat P-value Lower CI Upper CI

------------------------------------------------------------------------------

const 0.0048 0.0012 4.0973 0.0000 0.0025 0.0072

MktRF 1.0711 0.0276 38.879 0.0000 1.0171 1.1251

Equation: S1V5, Dependent Variable: S1V5

==============================================================================

Parameter Std. Err. T-stat P-value Lower CI Upper CI

------------------------------------------------------------------------------

const 0.0082 0.0013 6.5142 0.0000 0.0057 0.0106

MktRF 1.0538 0.0293 36.019 0.0000 0.9965 1.1111

Equation: S5V1, Dependent Variable: S5V1

==============================================================================

Parameter Std. Err. T-stat P-value Lower CI Upper CI

------------------------------------------------------------------------------

const 0.0032 0.0005 5.8787 0.0000 0.0021 0.0042

MktRF 0.9861 0.0126 78.376 0.0000 0.9615 1.0108

Equation: S5V3, Dependent Variable: S5V3

==============================================================================

Parameter Std. Err. T-stat P-value Lower CI Upper CI

------------------------------------------------------------------------------

const 0.0052 0.0007 7.4953 0.0000 0.0039 0.0066

MktRF 0.8472 0.0162 52.204 0.0000 0.8154 0.8790

Equation: S5V5, Dependent Variable: S5V5

==============================================================================

Parameter Std. Err. T-stat P-value Lower CI Upper CI

------------------------------------------------------------------------------

const 0.0051 0.0011 4.5167 0.0000 0.0029 0.0073

MktRF 0.9851 0.0263 37.515 0.0000 0.9337 1.0366

==============================================================================

Covariance Estimator:

Homoskedastic (Unadjusted) Covariance (Debiased: False, GLS: False)

Using GLS with common regressors¶

As noted previously, forcing GLS has no effect (except on changing the \(R^2\)). This can be seen below.

[30]:

print(mv_ols.fit(cov_type="unadjusted", method="gls"))

System GLS Estimation Summary

===================================================================================

Estimator: GLS Overall R-squared: 0.6564

No. Equations.: 6 McElroy's R-squared: 0.8776

No. Observations: 819 Judge's (OLS) R-squared: 0.6564

Date: Tue, Oct 21 2025 Berndt's R-squared: 0.9773

Time: 13:37:43 Dhrymes's R-squared: 0.6564

Cov. Estimator: unadjusted

Num. Constraints: None

Equation: S1V1, Dependent Variable: S1V1

==============================================================================

Parameter Std. Err. T-stat P-value Lower CI Upper CI

------------------------------------------------------------------------------

const -0.0020 0.0017 -1.1608 0.2457 -0.0054 0.0014

MktRF 1.3736 0.0403 34.101 0.0000 1.2947 1.4526

Equation: S1V3, Dependent Variable: S1V3

==============================================================================

Parameter Std. Err. T-stat P-value Lower CI Upper CI

------------------------------------------------------------------------------

const 0.0048 0.0012 4.0973 0.0000 0.0025 0.0072

MktRF 1.0711 0.0276 38.879 0.0000 1.0171 1.1251

Equation: S1V5, Dependent Variable: S1V5

==============================================================================

Parameter Std. Err. T-stat P-value Lower CI Upper CI

------------------------------------------------------------------------------

const 0.0082 0.0013 6.5142 0.0000 0.0057 0.0106

MktRF 1.0538 0.0293 36.019 0.0000 0.9965 1.1111

Equation: S5V1, Dependent Variable: S5V1

==============================================================================

Parameter Std. Err. T-stat P-value Lower CI Upper CI

------------------------------------------------------------------------------

const 0.0032 0.0005 5.8787 0.0000 0.0021 0.0042

MktRF 0.9861 0.0126 78.376 0.0000 0.9615 1.0108

Equation: S5V3, Dependent Variable: S5V3

==============================================================================

Parameter Std. Err. T-stat P-value Lower CI Upper CI

------------------------------------------------------------------------------

const 0.0052 0.0007 7.4953 0.0000 0.0039 0.0066

MktRF 0.8472 0.0162 52.204 0.0000 0.8154 0.8790

Equation: S5V5, Dependent Variable: S5V5

==============================================================================

Parameter Std. Err. T-stat P-value Lower CI Upper CI

------------------------------------------------------------------------------

const 0.0051 0.0011 4.5167 0.0000 0.0029 0.0073

MktRF 0.9851 0.0263 37.515 0.0000 0.9337 1.0366

==============================================================================

Covariance Estimator:

Homoskedastic (Unadjusted) Covariance (Debiased: False, GLS: True)